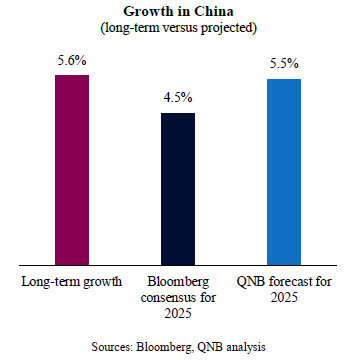

After the re-opening from the late wave of Covid pandemic in China two years ago, there was significant hope for another period of strong Chinese driven global growth. However, following an initial recovery, expectations faded as GDP prints came consistently below the country’s long-term average of 5.6%. Part of the reason for a lacklustre performance in recent quarters has been the lack of major fiscal stimulus and the lack of clarity in terms of overall policy direction.

Last month, Chinese economic authorities decided to take more decisive action to support growth. A new battery of policy stimulus measures were launched. This included the re-capitalization of state banks, cuts in interest rates and reserve requirement ratios, more fiscal spending, and support for both real estate and capital markets.

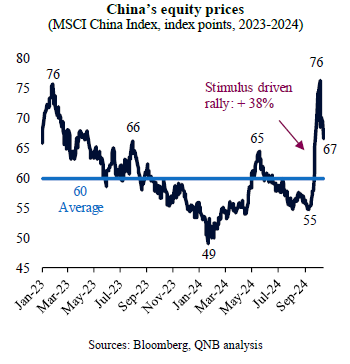

The announcement quickly reignited the risk-taking “animal spirits” of investors, speculators and entrepreneurs. This led Chinese asset prices to surge significantly, with equity prices up 38% in a matter of three weeks, before softening and stabilizing. Importantly, as concerns emerged about whether the announcement would be enough to spur stronger growth, there was guidance that the government is willing to deploy more measures should it be needed for growth or financial stability.

Despite the initial reaction from markets, analysts are still questioning to what extent the Chinese government is committed to large, sustained supportive interventions, and whether this would have a strong spill over on consumer sentiment and real activity. At the time of writing, analyst projections are still modest and do not reflect a material change in growth expectations. This is well captured by the Bloomberg consensus, a tool that tracks forecasts from economists, think tanks and research houses, presenting a range of projections as well as the median point of market expectations for growth in a given country. The Bloomberg consensus forecasts point to tepid 4.8% and 4.5% Chinese growth in 2024 and 2025.

There is nonetheless scope for significant upward revisions in Chinese growth expectations to 5.5%, more aligned with GDP potential. Two main factors sustain our position.

Growth in China

First, the new round of stimulus suggests that policymakers are concerned about growth and committed to support it. Moreover, it also suggests that the announced GDP target of 5% is still a key KPI that should be achieved. In the recent past, there were concerns that the main economic KPIs for the Chinese government were associated with the technological roadmap, i.e., raising in the value chain of strategic sectors like space, AI, and quantum communications and computing. As deploying the “bazooka” or enacting “massive stimulus” is no longer off-limits and indeed needed for the desired growth target achievement, we expect even further easing measures in the near future, creating a solid footing to the economic expansion.

Second, the start of a “global easing cycle” in which major central banks cut policy rates is also favourable for China. This enables more aggressive economic policy actions by Chinese authorities, particularly the PBoC. As the US Fed cuts rates further, the PBoC will have more policy room to ease without creating additional incentives for capital outflows from China. In recent years, the US-China interest rate differential changed dramatically in favour of the US, with higher US yields attracting capital inflows from the rest of the world, including China. This created pressure in the renminbi, which depreciated by 13% since its recent peak in February 2022. A US Fed easing cycle should unlock more monetary stimulus from the PBoC, providing a tailwind for the Chinese economy. Lower policy rates allows for more liquidity and credit growth, favouring the return of private and provincial investments. This should also provide relief for indebted entities and provide a boost to consumer sentiment.

All in all, more positive market sentiment, a firmer commitment from the Chinese government for stronger growth, and more monetary policy room for rate cuts should favour a faster GDP expansion of 5.5% in 2025.

Download the PDF version of this weekly commentary in English or عربي