Commodities are one of the pillars of the global economy, vital for real world, tangible, physical activities, such as transportation and the production of manufactured goods. Copper, in particular, as the most widely traded base metal, has a prominent role within the commodity complex. An efficient electrical conduit, copper is critical for a broad range of industries, including construction, real estate, infrastructure, automotive, and white goods.

Copper prices are often a helpful foretell of the direction of investments and the business cycle, giving quality macro and sectoral insights. Hence, investors and analysts commonly refer to the commodity as “Dr. Copper,” as if it had a PhD in economics.

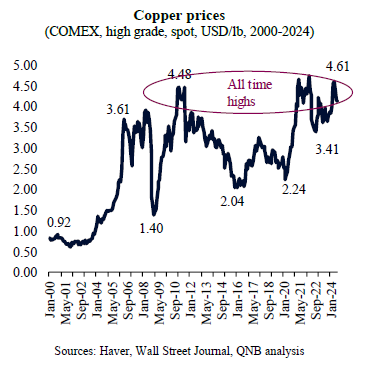

Copper prices are again hovering around the all time high range of USD 4.1-4.6 per pound (lb), reached both after the Global Financial Crisis (GFC) and the post-Covid investment boom. This naturally raises the question of whether copper prices are too high, requiring a significant correction, or prone to a meaningful breakout towards much higher prices for a sustained period.

Although copper prices are currently at historical highs, we recognize the volatility of prices as well as the fact that both headwinds and tailwinds are relevant. In terms of headwinds, the impact on copper demand from slower urbanization and real estate woes in China is important. During the early 2000s until the end of the recovery from the GFC, strong Chinese growth was indeed the most important factor supporting higher copper prices. In recent years, however, other factors have been prevailing. In our view, these new factors or tailwinds are expected to more than offset headwinds coming from China, creating a bullish environment for the long-term. In this article, we identify three main tailwinds that should support higher copper prices over the next several years.

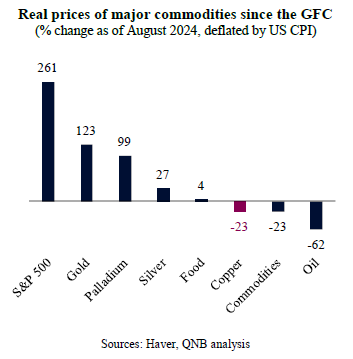

First, several measures of relative prices suggest that there is significant room for higher copper prices in the future. In fact, copper prices are down 23% in real terms (discounted by US CPI inflation) since the GFC in 2008, versus real gains for other metals, such as gold, palladium and silver. Copper’s performance is more aligned with the overall performance of major commodity indexes, which suffered significantly as well with real declines in energy prices.

Second, basic fundamentals suggest extended periods of copper shortage over the medium- and long-term, which should propel prices. On the demand side, physical needs for copper are set to more than double from current levels to more than 50 million metric tons over the next decade. This is mostly due to strong prospects associated with the “green agenda,” such as the increase in the supply of electric vehicles, the build-up of new power infrastructure, and renewable energy projects, which are all intensive in copper consumption. As a metal with unique properties for electrical conductivity, copper will play a critical part in clean energy build out. In contrast, supply growth is expected to be severely limited in the coming years. Inventories were drawn down to historically low levels and capital spending in the mining industry continues to go down vis-à-vis total copper sales or asset depreciation. Major copper miners have been reluctant to increase CAPEX on new exploration projects, due to lengthy licensing and regulatory burdens, resource nationalism in production countries, and shareholder demands for more capital discipline. As a result, supply should take a long time to meet the incoming demand, likely requiring higher copper prices.

Third, foreign exchange (FX) movements are also likely to play their part in supporting copper prices. Historically, copper prices are negatively correlated with the USD, with copper prices going up when the USD is down and vice versa. An assessment of the USD suggests that the currency is overvalued by around 9%, requiring a significant adjustment. A cheaper USD increases the purchasing power of the rest of the world for USD-priced commodities, such as copper, boosting overall demand and supporting prices.

All in all, despite weakness in demand from China, copper prices are expected to be well supported by relatively low prices, a bullish imbalance of supply-demand and a much-expected USD adjustment.

Download the PDF version of this weekly commentary in English or عربي